Tax tables

Please talk to us about your tax returns and tax planning

Tax years

- Click Section 1. to 10. headings to close/open details

2015/16

£

2016/17

£

Section 1 - Income tax rates, General and Dividend rates

Income tax rates - (non-dividend income)

0% lower rate tax - savings rate only

Does not apply if all income exceeds the personal allowance when the normal Basic, Higher or Additional rate applies

But there is the Personal savings tax free allowance

Up to 5,000

Up to 5,000

20% basic rate tax band

Up to 31,785

Up to 32,000

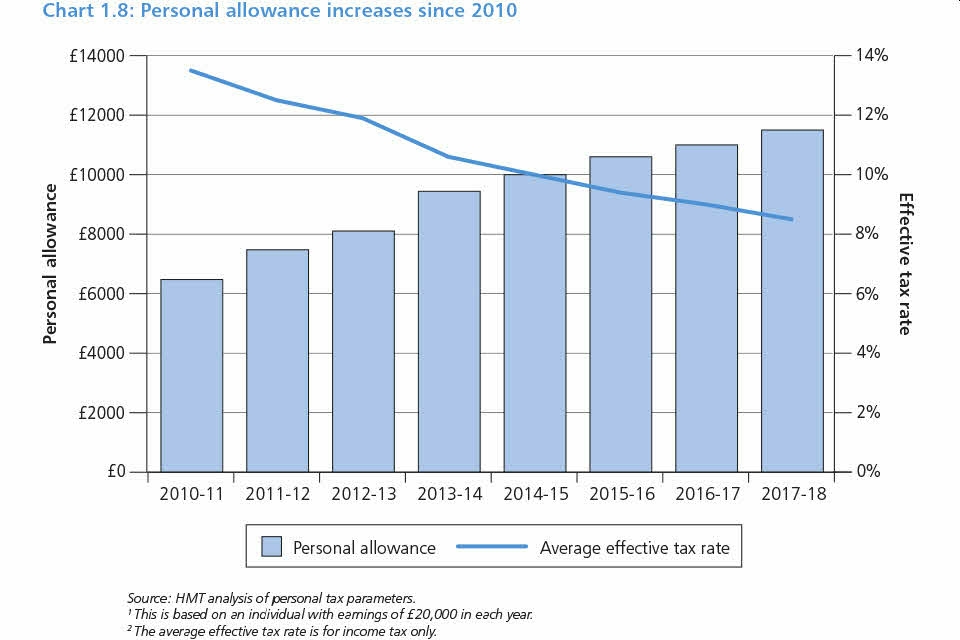

Normal Personal allowance

but some National Insurance is payable on PAYE of this amount

10,600

11,000

Higher rates apply to the basic rate band plus the personal allowance.

Add to this figure: your Gross pension contributions and Gift Aid Charitable donations

Additional income at higher rates.

42,385

43,000

40% Higher rate tax band

31,786 to 150,000

32,001 to 150,000

45% Additional rate tax

Above 150,000

Above 150,000

Personal allowance Income limit – abatement for excess earnings: £1 for every £2

100,000

100,000

Personal allowance Income limit – No personal allowance with income in excess of:

121,200

122,000

From 2008-09 to 2014-15 a 10% starting rate applied up to £2,880 to savings income only and did not apply if non-savings income exceeded the threshold.

Income tax rates - (dividend income old rules to 5/4/2016)

10% rate

Up to 31,785

n/a

32.5% higher dividend rate tax band

31,786 - 150,000

n/a

37.5% additional dividend rate tax

Above 150,000

n/a

Up to 5/4/2016 net dividends appear in the company accounts; gross dividends are used for personal tax computations with a 10% notional tax credit.

Income tax rates – (dividend income new rules from 5/4/2016)

0% rate

n/a

Up to 5,000

7.5% basic dividend rate tax band

n/a

5,001 - 32,000

32.5% higher dividend rate tax band

n/a

32,001 – 150,000

38.1% additional dividend rate tax

n/a

Above 150,000

From April 2016:

⚫ The notional 10% tax credit on dividends is abolished:

There is no net and gross, all dividends being gross.

The figure in the company accounts is equivalent to the figure used for personal tax computations.

⚫ Foreign dividends are taxed on the net amount:

Foreign dividends will no longer qualify for UK dividend tax credits and there will no longer be the need to gross-up any qualifying dividend when working out the UK tax due.

There is no amount claimable for foreign tax deductions.

⚫ Remittance basis: Special Withholding Tax SWT treatment is not affected by this.

Construction Industry Scheme CIS deductions

Construction industry subcontractors registered under the CIS scheme - deduction from gross labour earnings

20%

20%

Construction industry subcontractors not registered under the CIS scheme - deduction from gross labour earnings

30%

30%

Construction Industry Scheme CIS deductions are deducted from net self employed or Corporation tax liabilities when the sub contractor claims them in his or her annual SA100 Self Assessment or CT600 Corporation tax return; any excess deduction is refunded by HMRC.

Section 2 - Personal allowances, Transferable tax allowance, Child benefit rates, Residential property, Micro entrepreneurs

Personal allowances

Personal allowance those born after 5 April 1948; – note 2.

but some National Insurance is payable on PAYE of this amount

10,600

11,000

Income limit – For personal allowance £1 for every £2 abatement note 1.

100,000

100,000

Income limit – No personal allowance with income in excess of:

121,200

122,000

Maximum tax and national insurance free pay - NI cumulative basis for directors only (per year)

8,060

8,060

Transferable married allowance; from 5 April 2015 backdateable

You apply online and you need both partners' National Insurance numbers and

Idetification information from passport, or your bank, or P60, or three payslips; see online guidance.

1,060

1,100

The transferor must earn less than:

9,540

9,900

The transferee must earn less than: Higher rates normally payable on additional earnings in excess of this figure.

42,385

43,000

Age related allowances now mainly discontinued:

Personal allowance those born between 6 April 1938 and 5 April 1948 – note 2.

10,600

n/a

Personal allowance those born before 6 April 1938 – note 3.

10,660

n/a

Married couple’s allowance those born before 6 April 1935 – note 2.

8,355

8,355

Married couple’s allowance – minimum amount – note 3.

3,220

3,220

Income limit for personal allowances (born before 6 April 1948)

27,700

n/a

Blind person's allowance

2,290

2,290

Transferable tax allowance for married couples and civil partners first year 2015/16

1,060

1,100

Starting Rate for Savings (SR) 0% starting rate Tax free savings income

Personal allowances unused after non savings income provide tax relief for savings income

up to 5,000

up to 5,000

Personal savings allowance for Basic rate tax payers – note 4.

n/a

1,000

Personal savings allowance for Higher rate tax payers – note 4.

n/a

500

Personal savings allowance for Additional rate tax payers – note 4.

n/a

nil

note 1. Abatement of personal allowance will apply of £1 for every £2 of taxable income in excess of income limit.

note 2. From 2016-17 onwards, all individuals will be entitled to the same personal allowance, regardless of the individuals’ date of birth. This allowance is subject to the £100,000 income limit which applies regardless of the individual’s date of birth.

note 3. This allowance is subject to the £27,700 income limit. The individual’s married couple’s allowance is reduced by £1 for every £2 above the limit. That reduction only applies after any reduction to their personal allowance. The relief for this allowance is given at 10%.

note 4. Basic rate tax is not deducted from personal savings interest from 2016-17 onwards.

Child benefit/Guardian's allowance rates

Higher rate (eldest child only) (per week)

20.70

20.70

Other children (per week)

13.70

13.70

Guardian's allowance (per week)

16.55

16.55

High income child benefit charge

Higher income per year of either partner - no - 0% of Child Benefit repayable

50,000

50,000

Higher income per year of either partner - all - 100% of Child Benefit repayable

60,000

60,000

Between the two: Excess income as a percentage of the difference

e.g. £51,000 is a £1,000 excess which, of £10,000, is 10% of Child Benefit repayable

% of 10,000

% of 10,000

High income child benefit charge - An income tax charge will apply to taxpayers with income exceeding £50,000 in a tax year, when child benefit is also received by them or their partner. The charge will reduce the financial benefit of receiving child benefit for those with income between £50,000 and £60,000 and remove it completely for taxpayers with income above £60,000.

Residential property letting allowances

Rent-a-room relief - When renting in the property where you are living at the time

4,250

7,500

Wear and tear of furnishings

- including kitchenware and appliances

- excluding boilers and radiators

10% of rent; when not claiming actual expenditure

nil; claim actual expenditure

Mortgage interest up to the original cost of the property

100%

100%

75% from 2017/18

There is a progressive reduction in Mortgage interest tax relief from highest rate tax allowance to basic rate tax allowance over tax years 2017/18 to 2020/21.

This does not apply to semi-commercial property, such as a shop with a flat above it; let together.

Reduction in Mortgage interest relief from highest rate tax allowance -

Applies to:

Does not apply to:

2016/17 - 100% at highest rate tax allowance,

2017/18 - 75%,

2018/19 - 50%,

2019/20 - 25%,

2020/21 - 0%

In 2020/21 all mortgage interest tax relief is given at basic rate, currently 20%.

This has no effect if the taxpayer, anyway, is paying only basic rate tax.

⚫ Individual

⚫ Non-UK resident individual

⚫ Partnership

⚫ Trust

⚫ UK resident companies

⚫ Non-UK resident companies

⚫ Furnished holiday lettings

Basic rate tax normally applies to total income up to:

42,385

43,000

Micro entrepreneurs allowance:

Micro entrepreneurs allowance - aimed at online activity but available generally

n/a

Allowance - £ 1,000

Individuals making property or trading incomes below the level of the allowance no longer need to declare the income or pay tax, while those who exceeded the level, from a separtate trading activity, can benefit by simply deducting the allowance instead of calculating their exact expenses.

The key word is INCOME, this is gross income; not profit. If gross income is above £1,000 you need to declare the income and may claim £1,000 instead of claiming actual expenses.

Section 3 - National insurance

National insurance

Class 1 - Lower earnings limit LEL, primary Class 1, minimum earnings to qualify for State pension and payroll benefits - set up a PAYE scheme at this level (per week)

112

112

Class 1 - Lower earnings limit LEL, primary Class 1

applied on a weekly basis, except for directors (per year)

5,824

5,824

Class 1 - Primary threshold PT, Employees start paying NI above this point, (per week)

155

155

Class 1 - Primary threshold PT - Employee's deductions - maximum tax and national insurance free pay - NI cumulative basis for directors only (per year)

8,060

8,060

Class 1 - Employee's primary rate between primary threshold and upper earnings limit

12%

12%

Class 1 - Upper earnings limit UEL primary, employees pay a lower rate of NI above this point, (per week)

815

827

Class 1 - Employee's primary rate above upper earnings limit UEL

2%

2%

Class 1 - Apprentice upper secondary threshold (AUST) for under 21s/ 25s

815

827

Class 1 - Secondary threshold ST(per week) - Employers start paying NI above this point

156

156

Class 1 - Employer's secondary rate above secondary threshold

13.80%

13.80%

Class 1 - Employer's secondary rate above secondary threshold (contracted out)

10.40%

n/a

Employment allowance, deducted from employers NI (per year per employer) – note 2.

2,000

3,000

Married woman's reduced rate between primary threshold and upper earnings limit

5.85%

5.85%

Married woman's rate above upper earnings limit

2.00%

2.00%

Class 2 - Self employed rate per week (where profits are above the annual small profits threshold)

2.80

2.80

Class 2 - Self employed rate per year (where profits are above the annual small profits threshold)

145.60

145.60

Previously paid by direct debit, quarterly bill or annual claim, from 6th April 2016 the amount needs to be entered on self assessment annual tax returns 2016/17 and paid together with other tax and National insurance. Existing direct debits have been deactivated by HM Revenue & Customs. There was an announcement of abolition of Class 2 NI after 2017/18.

Class 2 - Self employed small profits threshold (per year)

5,965

5,965

Class 2 - Special rate for share fishermen (per week)

3.45

3.45

Class 2 - Special rate for volunteer development workers

5.60

5.60

Class 3 - voluntary contributions rate (per week)

14.10

14.10

Class 3 - voluntary contributions rate (per year)

735

735

Class 4 - Self employed lower profits limit - start paying NI above this point

8,060

8,060

Class 4 - Self employed rate between lower profits limit and upper profits limit

9.00%

9.00%

Class 4 - Self employed upper profits limit, pay a lower rate of NI above this point - per year

42,385

43,000

Class 4 - Self employed rate above upper profits limit

2.00%

2.00%

Employers further National Insurance liabilities

Class 1A National Insurance: expenses and benefits

Must be reported on Form P11D Expenses and benefits subject to £100 per month late filing penalty for up to twelve months after 6th July

13.8%

13.8%

Class 1B National Insurance: PAYE Settlement Agreements (PSAs)

13.8%

13.8%

note 1. From April 2016 employers of apprentices under the age of 25 will no longer be required to

pay secondary Class 1 (employer) National Insurance contributions (NICs) on earnings up to

the Upper Earnings Limit (UEL), for those employees.

note 2. From April 2016,companies where the director is the sole employee will no longer be able to claim the

Employment Allowance

Section 4 - PAYE; Pensions, Payroll benefits SSP, SMP and Student loan recovery, Minimum wage

Pensions

State pension income

The basic State Pension if you reached State Pension age before 6 April 2016 - per week

115.95

119.30

The new State Pension if you reached State Pension age on or after 6 April 2016 - per week

n/a

155.65

New State Pension paid pro rata by qualifying years; 10 years minimum; 10/35ths entitlement; 35 years maximum full entitlement.

If you defer drawing your State pension:

The basic State Pension is increased by 10.4% for each year you defer.

The new State Pension is increased by 5.8% for each year you defer.

Pro rata increases for periods of less than one year.

State Pension top up:

⚫ A man born before 6 April 1951; or a woman born before 6 April 1953.

⚫ You can make a contribution until 5 April 2017 - to receive up to £25 per week, index linked, for life.

⚫ Inheritable by spouse.

n/a

25.00

Private pension contributions

Annual allowance

40,000

40,000

Lifetime allowance

1,250,000

1,000,000

The Finance Bill 2015 provides that from tax year 2016/17 the annual allowance for those earning above £150,000 is to be reduced on a tapering basis so that it reduces to £10,000 for those earning above £210,000. For every £2 of income above £150,000, an individual’s annual allowance will reduce by £1.

Student loan recovery

Employee earnings threshold - Plan 1 the default - started a course of study before 1 September 2012 - gross pay

333.00 pwk

17,316 pa

336.00 pwk

17,472 pa

Employee earnings threshold - Plan 2 when advised by the tax office - started a course of study on or after 1 September 2012 - gross pay

n/a

403.00 pwk

20,956 pa

Student loan deductions on the amount in excess of the threshold

9%

9%

Payroll benefits

Employee vehicles: Mileage Allowance Payments (MAPs)

Car - first 10,000 miles - per mile

45 pence

45 pence

Car - subsequent miles - per mile

25 pence

25 pence

Motorcycle - per mile

24 pence

24 pence

Cycle - per mile

20 pence

20 pence

National Minimum Wage

Aged 25 and above (national living wage rate) from 1.4.2016 - per hour

n/a

7.20

National Minimum Wage

from

1.10.2015

£

from

1.10.2016

£

National Minimum Wage review date is 1.10.2016 then the next review date is 1.4.2017

Aged 21 to 24 - per hour

6.70

6.95

Aged 18 to 20 from 1.10.2015 - per hour

5.30

5.55

Aged over compulsory school age 17 - per hour

3.87

4.00

Apprentice rate - per hour

3.30

3.40

Section 5 - Reliefs and incentives, ISA's

Relief's and incentives

Enterprise Investment Scheme (EIS) - maximum

1,000,000

1,000,000

Venture Capital Trust (VCT) - maximum

200,000

200,000

Enterprise Management Incentive Scheme (EMI) - employee limit

250,000

250,000

Seed Enterprise Investment Scheme (SEIS) - maximum

100,000

100,000

Income tax relief on EIS schemes - Claim tax relief in the tax year you invest or the prior tax year

30%

30%

Income tax relief on VCT schemes - Claim tax relief in the tax year you invest only

30%

30%

Income tax relief on SEIS schemes - Claim tax relief in the tax year you invest or the prior tax year

50%

50%

Individual Savings Account (ISA):

New ISA (NISA) limits

New ISA (NISA) annual limit

15,240

15,240

New Junior ISA investment annual limit

4,080

4,080

New child value of Child Trust Fund annual limit

4,080

4,080

Section 6 - Capital gains tax, Inheritance tax and Taxation of trusts

Capital gains tax

Rate - basic rate tax payer – note 1

18%

10%

- higher rate tax payer – note 1

28%

20%

Rate - basic rate tax payer – Residential property

18%

18%

- higher rate tax payer – Residential property

28%

28%

Higher rates apply to total annual income and capital gains above:

42,385

43,000

Two Additional reliefs on capital gains on a Residential property which has BOTH been your main residence AND has been let on a commercial basis

1. Private residence relief: Actual period of residence plus, in the period prior to disposal

1.5 Years

1.5 Years

2. Lettings relief: the Lower of Private residence relief or

40,000

40,000

Annual exemptions – individuals (per year)

11,100

11,100

Certain trusts for disabled persons (per year)

11,100

11,100

Other trusts (per year)

5,550

5,550

Entrepreneurs Relief lifetime limit

10,000,000

10,000,000

Entrepreneurs Rate

10%

10%

Chattels exemption - up to

6,000

6,000

note 1. The 2016/17 reduction does not apply to residential property (where not covered by Principal Private Residence Relief PPR Relief)

Inheritance tax IHT

Single persons nil rate band

1 - 325,000

1 - 325,000

Single persons 40% band

over 325,000

over 325,000

Married couples or civil partnerships allowance nil rate band

Any unused part of the Inheritance Tax IHT nil Rate Band NRB from a deceased spouse or civil partner may be transfered to the surviving spouse or civil partner.

650,000

650,000

Gifts to charities

Exempt

Exempt

Small gifts to same person

250

250

General gifts

3,000

3,000

Wedding gifts:

From: Parent

5,000

5,000

From: Grandparent/party

2,500

2,500

From: Other person

1,000

1,000

From 6 April 2012 a reduced rate of Inheritance tax IHT of 36% was introduced where 10% or more of the net estate is left to charity.

Business Property Relief

Business or interest in a business and transfer if unquoted shareholdings

100%

100%

Transfers out of a controlling shareholding in quoted companies, land and buildings, plant and machinery used in a qualifying company or partnership

50%

50%

Taxation of trusts

Accumulation or discretionary trusts:

Trust income up to £1,000 – dividend type income

10%

Not confirmed

Trust income up to £1,000 – all other income

20%

20%

Trust income over £1,000 – dividend type income

37.5%

Not confirmed

Trust income over £1,000 – all other income

45%

45%

Bare trusts:

Dividend type income

10%

Not confirmed

All other income

20%

20%

Section 7 - Corporation tax, Capital Allowances, Research and Development Tax Credit Rates and Patent Box

Corporation tax

All profits and gains (excluding determination agreements and diverted profits)

20%

20%

From 1st April 2015, Tax year 2015/16, the corporation tax rate has been unified, eliminating the previous higher rates and marginal relief for more profitable companies.

Overdrawn directors loan accounts:

Corporation tax payable by the company on overdrawn Directors' loan accounts s455

25%

32.5%

De minimis; balances below this may avoid s455 Corporation Tax providing they are repaid within nine months of the company year end.

5,000

5,000

Any balance may avoid s455 Corporation Tax if it is repaid within nine month of the company year end but the position may be difficult to dertermine where accounts are produced annually. Anti avoidance rules mean that the loan may not be retaken within certain time limits.

Subject to interest at official rates for balance exceeding

10,000

10,000

Beneficial loan arrangements - HMRC official rates

3.0% pa

3.0% pa

There is a taxable benefit to the borrower on the interest figure if interest is not paid

Employers further National Insurance liability on the interest figure if statutory interest is not paid by the borrower

Class 1A National Insurance: expenses and benefits

Must be reported on Form P11D Expenses and benefits subject to £100 per month late filing penalty for up to twelve months after 6th July

13.8%

13.8%

Family companies need to have funds in the company to pay Corporation tax, for the year, AT YEAR END even though it is not payable until nine months later. If not, there could be an overdrawn directors' loan account giving rise to a s455 liability. De minimis £5,000.

Corporation tax paid under s455 is reclaimed pro rata when the overdrawn directors loan is repaid in whole or in part.

Future Corporation Tax rates announced 16th March 2016

- Tax year

- From 1.4.2017 - 2017/18

- From 1.4.2018 - 2018/19

- From 1.4.2019 - 2019/20

- From 1.4.2020 - 2020/21

- Corporation tax rate

- 19%

- 19%

- 19%

- 17% an additional 1% cut

Capital Allowances

Main writing down allowance (reducing balance)

18%

18%

Special rate writing down allowance (reducing balance)

Applies to cars with CO2 emissions of more than 130g/km and other specific assets

8%

8%

First year allowances for certain energy-saving/water efficient products

100%

100%

Annual investment allowance

You may claim this on all assets, except cars, including Special rate other specific assets

100%

100%

AIA level set permanently from 1 January 2016 at £200,000 pa

Research and Development Tax Credit Rates

SME Rate

230%

230%

Large company rate

130%

130%

Large companies expenditure credit scheme (LCEC) scheme

10%

n/a

Research and development expenditure credit (RDEC) scheme

n/a

11%

The RDEC scheme replaces the LCEC scheme from April 2016

Patent Box

Patent box

10%

10%

The Patent box regime was phased in from April 2013 with companies able to claim the benefit of 60% for 2013/14, 70% for 2014/15, 80% for 2015/16, 90% for 2016/17 and 100% from 2017/18 onwards

Section 8 - VAT

VAT

Standard rate

Check VAT flat rates, by business type, 4% to 14.5%, using the link to the right.

20%

20%

Reduced rate

5%

5%

Zero rate

0%

0%

Normal scheme registration threshold.

Sales, excluding VAT, which exceed the threshold in ANY twelve month period, not just at year end

82,000

83,000

Deregistration threshold excluding VAT; calculate on the latest twelve month period.

The deregistration application is a postal process:

Complete and post Form VAT7: application to cancel your VAT registration.

HM Revenue & Customs confirm your effective date of deregistration.

Deregistration is complete after a final concluding VAT return - filed online.

80,000

81,000

Flat rate scheme – maximum taxable turnover, excluding VAT, allowed to join

150,000

150,000

Flat rate scheme exit threshold - maximum equivalent taxable turnover excluding VAT required to leave

191,667

191,667

Flat rate scheme – maximum equivalent taxable turnover, including VAT, allowed to join

180,000

180,000

Flat rate scheme exit threshold - maximum taxable turnover including VAT required to leave

230,000

230,000

Flat rate scheme - claim VAT on asset purchases in excess of, excluding VAT

2,000

2,000

Cash accounting scheme -maximum to join excluding VAT

1,350,000

1,350,000

Cash accounting scheme - exit threshold excluding VAT

1,600,000

1,600,000

Annual accounting scheme – maximum to join excluding VAT

1,350,000

1,350,000

Annual accounting scheme – exit threshold excluding VAT

1,600,000

1,600,000

Flat rate scheme "equivalents" above will change if the VAT rate changes from .

Cash accounting and Flat rate entry and exit criteria are based on your reasonable expectations about what is likely to happen in the following twelve months.

Annual accounting entry criteria is also based on your reasonable expectations about what is likely to happen in the following twelve months.

Annual accounting exit criteria: you must leave if your taxable turnover is (or is likely to be) above the exit threshold at the end of the annual accounting year.

Stamp Duty on shares and securities

Not normally payable if you buy stocks and shares for £1,000 or less

0.5%

0.5%

Rounded up to the nearest £5

Send your stock transfer forms and stamp duty payable to the Stamp Office no later than 30 days after they’ve been dated and signed. Subject to late submission penalties.

Stamp Duty Land Tax SDLT

Residential properties: new regime from 3rd December 2014

Band: market price £

From 1st April 2016 - Applicable when exemptions apply: replacing your main residence or buying your only-property for any purpose.

Incremental

by band

Incremental

by band

HMRC tests of main residence:

⚫ Where the individual and their family spends their time;

⚫ If the individual has children, where they go to school;

⚫ At which residence the individual is registered to vote;

⚫ Where the individual works;

⚫ The location and degree of furnishing and location of moveable possessions; and

⚫ The correspondence and registration addresses given to various organisations.

0 - 40,000

0%

0%

0 - 125,000

0%

0%

125,001 – 250,000

2%

2%

250,001 – 925,000

5%

5%

925,001 -1,550,000

10%

10%

1,500,001 and over

12%

12%

Rental properties and second homes: Additional residential properties Higher rates + 3%: new regime from 1st April 2016

Band: market price £

- Applicable in all other circumstances where the above exemptions do not apply.

Applicable if you buy your first main residence when you own another property,

Applicable whether the other property is in UK or not.

You pay the extra 3% when the result is that you own two properties.

If you dispose of your previous main residence within 3 years you may be eligible for a refund of the additional 3%.

If you sell your main residence and buy a new main residence within 3 years you do not pay the extra 3% even though you may own other properties at the time of buying the second main residence.

n/a

Incremental

by band

after adding 3%

0 - 40,000

-

0%

0 - 125,000

-

3%

125,001 – 250,000

-

5%

250,001 – 925,000

-

8%

925,001 – 1,500,000

-

13%

1,500,001 and over

-

15%

Non-residential property: new regime from 17th March 2016

Band: market price £ Non-residential.

Including semi-commercial property, such as a shop with a flat above it; bought together.

Slab basis

to 16.3.2016

Incremental

by band

0 - 150,000

0%

0%

150,001 - 250,000

1%

2%

Over 250,000

3%

5%

Over 500,000

4%

n/a

Annual Tax on Enveloped Dwellings (ATED) when a company owns a residential property valued at more than £500,000

on 1 April 2012, or at acquisition if later

More than £0.5m but not more than £1m

n/a

£3,500

More than £1m but not more than £2m

£7,000

£7,000

More than £2m but not more than £5m

£23,350

£23,350

More than £5m but not more than £10m

£54,450

£54,450

More than £10m but not more than £20m

£109,050

£109,050

More than £20m

£218,200

£218,200

Annual Tax on Enveloped Dwellings (ATED) is payable by the company or other non-natural persons NNP's.

Non-natural persons NNP's include partnerships and all collective investment schemes.

UK Insurance Premium Tax

Announced in the budget on 8th of July 2015, an increase to UK Insurance Premium Tax from 6.0% to 9.5%, effective from the 1st of November 2015

Up to 31st October 2015

6.0%

-

After 1st of November 2015

9.5%

9.5%

ACCA LEGAL NOTICE

This is a basic guide prepared by ACCA UK's Technical Advisory Service for members and their clients with additional content added by V.G. Woodhouse & Co. It should not be used as a definitive guide, since individual circumstances may vary. Specific advice should be obtained, where necessary.