Our Services

Or call us

☎ 020 8810 4500 ![]()

I look forward to hearing from you

Vic Woodhouse

Ealing

London

W5 2PJ

Accountancy

Complete professional accounting services. Including auditing and Solicitors Accounts Rules. Limited companies and PLC's, self employed sole traders and partnerships. Dormant company accounts and taxation. Avoid Companies House and tax penalties.

Read more

about accountancy

Tax returns and tax advice

Tax advice; pay the right tax and organise your affairs legitimately to minimise tax. Avoid or deal with tax inspections and enquiries. Property tax. Avoid personal and Corporation Tax penalties.

Read more

about tax

Company formation and registration

Company formation and registration; new business startup and formation of a company. Professional limited company formation agents. Company secretary and ltd company secretarial services.

Read more

about companies solutions

Bookkeeping and VAT

Bookkeeping; keep your VAT up to date with online filing. Build up the right records for your final accounts. See our Client bookkeeping guide or call our Bookkeepers helpline. Avoid or guard against Tax and VAT enquiries.

Read more

about bookkeeping and VAT

Payroll and CIS services

Payroll; full professional payroll Construction Industry Scheme CIS and National Insurance service. Avoid PAYE and Construction industry scheme CIS penalties.

Read more

Find out about payroll and CIS

Open Banking

Get your banking data to us in minutes using the hard-won freedom to access your own banking data for your own purposes.

Online Accounting Software and Bookkeeping for Small Businesses

Our simple and effective online accounting software and bookkeeping fully supported; secure with no long term commitment.

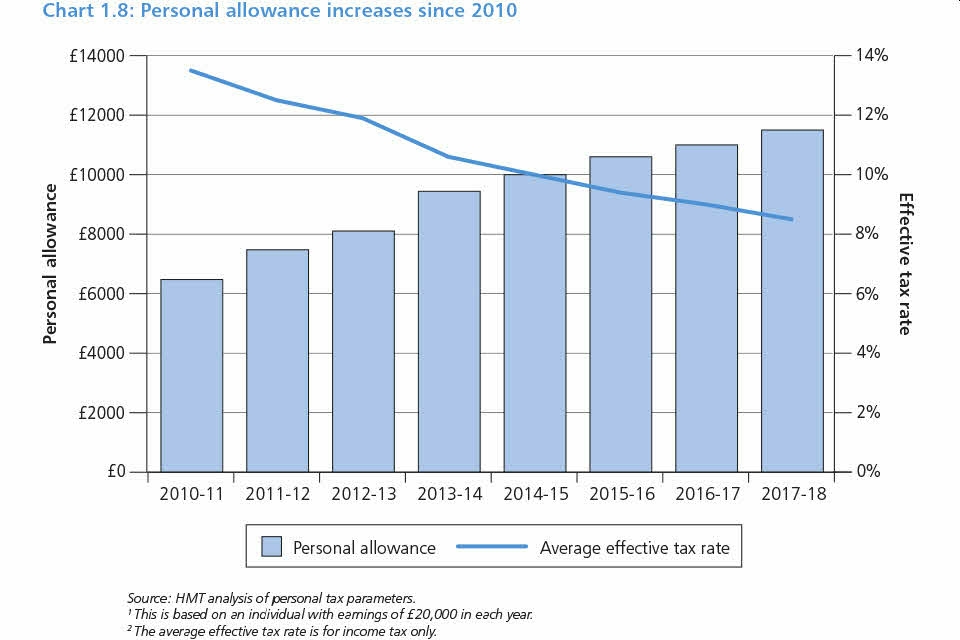

Tax tables

Check your tax against the latest tables:

Income tax, tax on dividends, Personal allowances, National insurance, Pensions contributions, Tax incentives, ISA's Individual Savings Accounts, Capital gains tax, Working tax credit and Childcare element, Child tax credit, Inheritance tax, VAT, Corporation tax, Stamp duty land tax, Trust Taxation, Capital Allowances, Research and Development Tax Credit Rates, Patent Box.

Tax Savings

Paying the right amout of tax could lead to tax savings. We will do our best.

Business Rescue and Recovery

- Talk to us about Business Rescue and Recovery:

- We will introduce an Insolvency Practitioner if necessary

- Limited company - Members Voluntary Liquidation

- Limited company - Creditors Voluntary Liquidation

- Personal bankruptcy

Audit and compliance

- Talk to us about your audit:

- This may be voluntary or compulsory

- Limited company

- Public Limited Company PLC

- Charity.

- and other compliance requirements:

- Renewable Transport Fuel Obligation - RTFO Verifier's Assurance Report.

Discover our comprehensive accounting services in Ealing, tailored to meet the needs of individuals and businesses.

Comprehensive accounting services in Ealing

Government COVID-19 Business Support

Limited companies, self employed, partnerships and other Self Assessment

services

Bounce Back Loans

Britain’s small businesses will be able to apply for quick and easy-to access loans of up to £50,000 – with the cash expected to land within days.

- The basics:

- Borrow an amount up to 25% of your sales 1st January 2019 to 31st December 2019.

- If you started after 1st January 2019: your estimate of sales for the first full year of business.

- Between £2,000 minimum and £50,000 maximum.

- No repayments for twelve months.

- Government pays the interest for twelve months.

- Then repayments start according to your agreement with the Bank.

- Repayments can be over a total period of five years.

- After the first twelve months interest is fixed at 2.5% per annum.

- You can make early repayment at no extra cost.

- Apply:

- Apply to your Bank or any Bank listed below.

- Banks will encourage online applications.

- Otherwise contact in the normal way.

- If you only have a personal bank account you may need to convert this to a business account.

- In most cases the money will arrive in your account one business day after the loan is approved.

- You can use a Bounce Back loan to repay other debt with your bank but the Bank may make you a lower priority in these circumstances. So it may take longer to process.

- The loan is 100% guaranteed by the Government.

- Banks offering Bounce Back Loans:

- Barclays.

- Clydesdale Yorkshire Bank Group.

- Danske Bank.

- Lloyds Bank.

- NatWest.

- Santander.

- Royal Bank of Scotland.

- Ulster Bank.

Government guidance - but look mainly at your Bank's guidance

Bounce Back Loans

Self-Employment Income Support Scheme

If you're self-employed or a member of a partnership and have been adversely affected by coronavirus (COVID-19) find out if you can use this scheme to claim a grant.

- What you can claim - The grant

- Average annual trading profits, by tax year, for your self-employed income.

- Divide by 12 months.

- Multiply by 3 months.

- x 80%

- = The amount you will receive is 80% of the lost income calculation for three months.

How to claim

HMRC aim to contact you by mid May 2020 if you’re eligible, to invite you to claim using the GOV.UK online service. Payment will be made by early June 2020 if your claim is approved.

- To claim:

- Confirm to HMRC that your business has been adversely affected by coronavirus.

- Presumably you will need to make an assessment of business lost.

- Taking into account actual income and expenditure from whatever trading activity you have been able to undertake.

- Be below state aid limits - this will be assumed.

- Have available:

- Unique Taxpayer Reference UTR.

- National Insurance number.

- Government Gateway user ID and password Guidance on applying

We will be pleased to help but Accountants cannot make a claim on behalf of their clients. - Bank account details.

- There will be immediate notification of approval.

- Funds will be paid into your bank account within six working days.

- This is taxable income equivalent to sales for your 2020/21 tax return due for filing between 6th April 2021 and 31st January 2022.

- This is self employed income for Universal Credit purposes.

- This is working sixteen hours per week for any tax credit claims.

- Apply for a Government Gateway

- You first enter your email address.

- You get back a confirmation code which you use to move forward with the application.

- Have available:

- Unique Taxpayer Reference UTR - if you have one.

- National Insurance number.

- Driving license or passport details to link you into other Government records.

- There are various security checking options; you have to choose two. The driving license and passport options are the most straight-forward.

- Telephone number.

- You need to be ready to receive text or email security numbers from HMRC.

- Apply: "Create sign in details" on the Sign in screen.

- You get a Government Gateway number.

- Set the Password.

- You are then ready to use the Government Gateway

- To make the claim; the additional detail you need is your bank account number and branch sort code.

| Self employed profit per annum average | Claim Subject to the total average of property, pension and other non trading income not exceeding self employed income |

|---|---|

| £0 to £37,500 | 80% of average profits for three months |

| £37,501 to £50,000 | £7,500 maximum |

| £50,001 upwards | Not eligible to claim |

- The three Applicable tax years for the Average trading profits calculation:

- Tax years: 2016/17, 2017/18, 2018/19.

- 2016/17 06/04/2016 to 05/04/2017

- 2017/18 06/04/2017 to 05/04/2018

- 2018/19 06/04/2018 to 05/04/2019

- The profit calculation is the same as on your tax return:

- Sales

- Less expenses

- Less capital allowances

- = The profit figure on which you paid tax

- If you had more than one trade, all trades are added together.

If not trading for three years

| Trading tax years | Basis of average profit calculation |

|---|---|

| 2017/18 and 2018/19 | The average of two years |

| If only trading 2018/19 | The one year |

| If not self employed until after 6th April 2020; 2020/21 | Not eligible to claim |

| If trading in 2016/17 but not 2017/18 and then trading again in 2018/19 | The average of all three years Which means two years of profit divided by three |

- Not eligible if:

- Average profits are more than £50,000

- Not eligible if:

- Average non trading income exceeds trading profit.

- Non-trading income

- The total of:

- Income from earnings normally PAYE.

- Property income.

- Dividends.

- Savings income.

- Pension income.

- Overseas income.

- Miscellaneous income (including taxable social security income).

How HMRC works it out - with examples and other information

How HMRC work out the Self-Employment Income Support SchemeGeneral description of the system

Check if you can claim a grant through the Self-Employment Income Support Scheme

All Personal Taxpayers - deferred on-account payment

Under Government special measures you may defer paying the 31st July 2020 on-account payment for the tax year 2019/20 until 31st January 2021

Without any late payment interest charge.

- On-account payments:

- With your 2018/19 tax, payable 31st January 2020, is a payment on-account for 2019/20.

- The 2019/20 on-account payment amount is arithmetic and calculated at 50% of the 2018/19 tax liability.

- An equal amount of 50% is payable 31st July 2020. It is this amout which may be deferred.

- We recommend filing your 2019/20 tax return during the summer so that you know your tax liability for 31st January 2021.

- This will include a payment on-account for 2020/21; calculated at 50% of the actual 2019/20 tax liability.

- Other information:

- No 2019/20 on-account payment will be due if you have a 2018/19 tax liability below £1,000.

- You may apply to reduce the on-account payment if 2019/20 tax is expected to be less than 2018/19 tax.

- Similarly, you may apply to reduce the on-account payment if 2020/21 tax is expected to be less than 2019/20 tax.

Full Government guidance

Understand your Self Assessment tax bill

Coronavirus (COVID19) VAT Deferral

- If you have VAT payments that are due between 20 March and 30 June 2020, you may choose to:

- Defer them without paying interest or penalties

- Pay the VAT due as normal

- You must continue to submit returns as normal.

- If you choose to defer their VAT payment, the VAT due must be paid on or before 31 March 2021.

- You do not need to tell HMRC that you are deferring VAT payments.

- Payments made by Direct Debit

- If you normally pay by Direct Debit you should contact your bank to cancel your Direct Debit as soon as you can, or you can cancel online if you’re registered for online banking.

Full Government guidance

https://www.gov.uk/guidance/deferral-of-vat-payments-due-to-coronavirus-covid-19

Coronavirus Job Retention Scheme - Furlough scheme

Key extracts from the Government guidance

- Who can claim

- You must have:

- created and started a PAYE payroll scheme on or before 19th March 2020.

- enrolled for PAYE online.

- a UK bank account.

- Any entity with a UK payroll can apply, including businesses, charities, recruitment agencies and public authorities.

- ...

- If you cannot maintain your current workforce because your operations have been severely affected by coronavirus (COVID-19), you can furlough employees and apply for a grant that covers 80% of their usual monthly wage costs, up to £2,500 a month, plus the associated Employer National Insurance contributions and minimum automatic enrolment employer pension contributions on that wage.

- You can furlough employees and apply for a grant that covers 80% of their usual monthly wage costs.

- For directors of their own companies paying 'minimum' under PAYE this would be the 2020/21 rate of £9,500

2020/21 £9,500 per annum (£183 x 52 weeks)

Furlough Claim:

£791.66 x 80% = £633.33 per month

taxable on the company for Corporation Tax

- Extended at reduced tapering pecentages to 31st October 2020.

- Now extend at 80% November 2020 until the end of March 2021.

- Employees can work part of the time.

- Reduce the furlough claim pro rata.

- Cap on the amount payable reduced pro rata.

| Month; claim by the 14th of the following month | Percentage furlough | Cap on amount payable |

|---|---|---|

| August 2020 | 80% | £2,500.00 |

| September 2020 | 70% | £2,187.50 |

| October 2020 | 60% | £1,875.00 | November 2020 to April 2021 | 80% | £2,500.00 |

Full Government guidance

https://www.gov.uk/guidance/claim-for-wage-costs-through-the-coronavirus-job-retention-scheme

Accounting service

Small Business Grant Fund SBGF

Small Business Grant Scheme for small business rate-payers

or 'rate-payers' subject to small business rate relief (SBRR)

The government will provide additional Small Business Grant Scheme funding for local authorities to support small businesses that already pay little or no business rates because of small business rate relief (SBRR), rural rate relief (RRR) and tapered relief. This will provide a one-off grant of £10,000 to eligible businesses to help meet their ongoing business costs.

Eligibility

Support for businesses that pay little or no business rates

- Grant £10,000.

- You are eligible if:

- on the 11 March 2020 you are eligible for Small Business Rate Relief (SBRR) Scheme.

- your business is based in England. Other schemes for Scotland, Wales and Northern Ireland.

- you are a business that occupies property.

- You cannot get Small Business Grant Fund SBGF for:

- Properties occupied for personal uses, such as private stables and loose boxes, beach huts and moorings.

- Car parks and parking spaces.

Support for businesses that pay business rates

- rateable value of up to and including £15,000.

- Grant £10,000.

- rateable value of over £15,000 and less than £51,000.

- Grant £25,000.

- How to access the scheme:

- Eligible businesses will be contacted by their local authority, though some local authorities have decided to operate an applications process.

- Any enquiries on eligibility for, or provision of, the grants should be directed to the relevant local authority.

Full Government guidance

Small Business Grant Fund

Companies House

Under Government special measures companies will be given additional support to help them meet their legal responsibilities.

- Striking off process suspended.

- Striking off process resumed from 10/10/2020. For more information please see our webpage https://www.vgwoodhouse.co.uk/company-formation/company-striking-off.htm

- Three month accounts filing extensions ‘automatic’.

- If you apply and

- If you cite COVID-19.

- You always need to apply before the normal due filing date.

- If you incur a late filing penalty:

- Appeals will be treated sympathetically if due to COVID-19.

Full Government guidance

https://www.gov.uk/government/news/companies-house-support-for-businesses-hit-by-covid-19

Companies House filing and company insolvency

Talk to us about the new legislation.

- Affected filings include:

- Accounts .

- Form CS01 Confirmation statement./li>

- Event-driven filings (changes to your company).

- Mortgage charges.

- Also additional important changes to:

- Corporate Insolvency.

- We are going into more detail about Private Companies,

- Limited Liability Partnerships LLP’s are the same.

- Please talk to us about Public Limited Companies PLC’s, Overseas companies and Societas Europaeas SE’s.

- Private Companies

- Where the company’s original filing date is between 27 June 2020 and 5 April 2021 the filing date will be extended by three months.

- The original date calculation will apply even if you have:

- Changed the company year end (accounting reference date ARD) or

- Have agreed an extension of the filing date with Companies House.

- If it is your company’s first accounts it will be the second anniversary of the registration date.

- New companies registered on or after 01/09/2019 and up to 05/07/2020 the accounts filing date is extended.

- New companies registered on or after 06/07/2020: Not extended; as normal, this is the end of the special extension period.

What normally applies:

| Year ended | Filing deadline Was: |

Extended to: |

New Company: 2nd anniversary of the reg. date. Extended to: |

|---|---|---|---|

| 30/09/2019 | 30/06/2020 | 30/09/2020 | 1 to 30/09/2020 |

| 31/10/2019 | 31/07/2020 | 31/10/2020 | 1 to 31/10/2020 |

| 30/11/2019 | 30/08/2020 | 30/11/2020 | 1 to 30/11/2020 |

| 31/12/2019 | 30/09/2020 | 31/12/2020 | 1 to 31/12/2020 |

| 31/01/2020 | 31/10/2020 | 31/01/2021 | 1 to 31/01/2021 |

| 29/02/2020 | 30/11/2020 | 28/02/2021 | 1 to 28/02/2021 |

| 31/03/2020 | 31/12/2020 | 31/03/2021 | 1 to 31/03/2021 |

| 30/04/2020 | 31/01/2021 | 30/04/2021 | 1 to 30/04/2021 |

| 31/05/2020 | 28/02/2021 | 31/05/2021 | 1 to 31/05/2021 |

| 30/06/2020 | 31/03/2021 | 30/06/2021 | 1 to 30/06/2021 |

| 31/07/2020 | 30/04/2021 | Not Extended | as normal This is the end of the special extension period |

| 31/07/2020 | New Company Extended | New company registered up to 05/07/2019 Extended 1 to 05/07/2021 |

|

| 31/07/2020 | New Company Not Extended | New company registered on or after 06/07/2019 Not Extended; 06 to 30/04/2020 as normal. This is the end of the special extension period. |